DEFINITION

An insurance premium is the amount of money the insurance company charges you for your insurance policy.

Key Takeaways

- The insurance premium is the amount of money you must pay to the insurance company for your insurance policy.

- Your insurance history, where you live, and other factors are used as part of the calculation to determine the insurance premium price.

- Insurance premiums will vary, depending on the type of coverage you are seeking.

- Getting a good price for your insurance premium requires you to shop around for an insurance company that’s interested in covering you.

- You’ll likely pay the premium on a monthly or annual basis.

How an Insurance Premium Works

Insurance costs money, but one term that may be new when you first start buying insurance is “premium.” Typically, the premium is the amount paid by a person (or a business) for policies that provide auto, home, health care, or life insurance coverage.

For example, if you pay $212 per month to keep your car insured, your yearly insurance premium would be $2,544. If you purchased a six-month policy, your insurance premium would be $1,272.

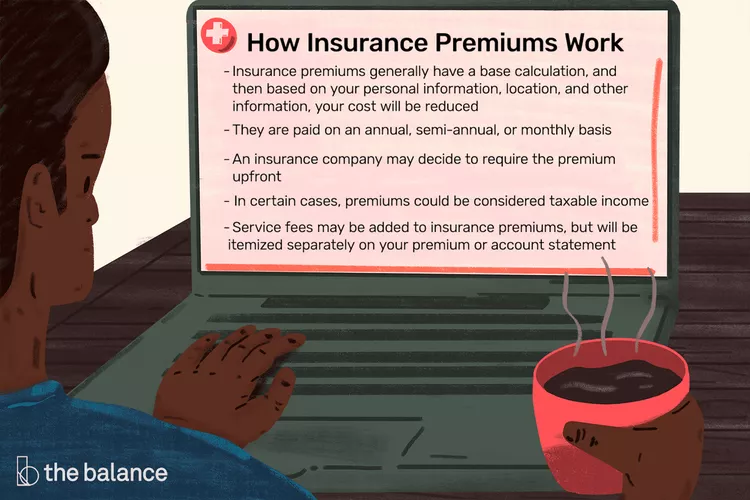

Insurance premiums usually have a base calculation. Then, based on your personal information and location, you may have discounts that are added to the base premium that reduces your cost. In order to get preferred rates, or more competitive or cheaper insurance premiums, additional information is used.

The insurance premium may be paid on an annual, semi-annual, or monthly basis. If the insurance company decides that it wants the insurance premium paid upfront, it may also require that.

Note

You may have to pay a premium upfront if you have ever had your insurance policy canceled for non-payment in the past.

The premium is the basis of your insurance payment. An insurance premium may be considered taxable income to you in certain cases (for example, coverage for group-term life insurance that exceeds $50,000 and is carried directly or indirectly by an employer).1

Service fees may also be added to your premium, depending on the local insurance laws and the provider of your contract. The National Association of Insurance Commissioners or your State Insurance Commissioners’ office can provide you with more information on your local regulations if you have a question about fees or charges on your premium.

Note

Any extra charges, such as issuance fees or other service charges, are not considered to be premiums and will be itemized separately on your premium or account statement.

The cost of your insurance premium will vary depending on the type of coverage you are looking for, as well as the risk.

This is why it is always a good idea to shop around for insurance or work with an insurance professional who can shop premiums with several insurance companies for you.

When people shop around for insurance, they may find different premiums charged for the cost of their insurance with different insurance companies, and they may save a lot of money on insurance premiums just by finding a company that is more interested in “writing the risk.”2

What Factors Determine an Insurance Premium?

An insurance premium is usually determined by four key factors.

1. Type of Coverage

Insurance companies offer different options when you purchase an insurance policy. The more coverage you get, or the more comprehensive coverage you choose, the higher your insurance premium may be.

For example, when looking at premiums for home insurance, if you purchase an open perils or all-risk coverage home insurance policy, it will be more expensive than a named perils home insurance policy that only covers the basics.3

2. Amount of Coverage and Your Insurance Premium Cost

Whether you are purchasing life insurance, car insurance, health insurance, or any other insurance, you will always pay a higher premium (more money) for higher amounts of coverage.

This can work in two ways. The first way is pretty straightforward, and the second way is a little more complicated but a good way to save on your insurance premiums:

First, your amount of coverage can be altered by the dollar value you want on whatever you are insuring. For example, insuring a house for $250,000 will be different from insuring a house at $500,000. It’s pretty straightforward: the more dollar value you want to insure, the more expensive the premium will be.

Second, you can pay less money for the same amount of coverage if you take a policy with a higher deductible. For example, with car insurance, you may be able to save up to 25% by increasing your deductible from $500 to $1,000, or something like that.4 In the case of health insurance or supplemental health policies, you can take higher deductibles or look at policies with different options like higher copays or longer waiting periods.

3. Personal Information of the Insurance Policy Applicant

Your insurance history, where you live, and other factors of your life are used as part of the calculation to determine the insurance premium that will be charged. Every insurance company will use different rating criteria.

Some companies use insurance scores, which can be determined by many personal factors, from credit rating to car accident frequency or personal claims history, and even occupation. These factors often translate into discounts on an insurance policy premium.

For life insurance, other risk factors specific to the person being insured will be used as well, such as age and health conditions.5

Note

Insurance companies have target clients, just like any business.

In order to be competitive, insurance companies will determine the profile of clients they want to attract, and they will create programs or discounts to help attract their target clients.

For example, one insurance company may decide that it wants to attract older adults or people who are retired as clients, while another may price premiums to attract young families or younger adults.

4. Competition in the Insurance Industry and Target Area

If an insurance company decides that it wants to aggressively pursue a market segment, it may deviate rates to attract new business. This is an interesting facet of insurance premiums because it may drastically alter rates on a temporary basis, or on a more permanent basis if the insurance company is having success and getting good results in the market.

Who Decides the Insurance Premium?

Every insurance company has people who work in various areas of risk assessment.

Actuaries, for example, work for an insurance company to determine:

- The likelihood of risks and perils

- The costs associated with the event of a disaster or claim, and then actuaries create projections and guidelines based on this information

Using the calculations, actuaries determine how much cost will be involved in paying claims as well as how much money the insurance company should collect in order to make sure it makes enough money to pay potential claims and also make a profit.

The information from the actuaries helps to shape underwriting. Underwriters are given guidelines to underwrite the risk, and one part of the task is to determine the premium.

The insurance company decides how much money it will charge for the insurance contract it is selling.

What Does the Insurance Company Do With Insurance Premiums?

The insurance company has to collect the premiums and make sure it saves enough of that money in liquid assets to be able to pay the claims for its policyholders.

The insurance company will take your premium and put it aside, letting it grow for every year you don’t have a claim. If it collects more money than what it pays in claim costs, operational costs, and other expenses, the company will be profitable.

Note

Earned premium is the portion of the total premium that an insurance company can show on its income statement as revenue, based on the policy’s duration and how much of the term has passed.6

Why Do Insurance Premiums Change?

In profitable years, an insurance company may not need to increase insurance premiums. In less-profitable years, if an insurance company sustains more claims and losses than anticipated, then it may have to review its insurance premium structure and re-assess the risk factors in what it is insuring. In cases like those, premiums may go up.

Examples of Insurance Premium Adjustments and Rate Increases

Have you ever spoken to a friend who was insured with one insurance company and heard them say what great rates they have, but then compared it with your own experience with the prices for the same company, and had it be completely different? This could happen based on various personal factors, discounts, or location factors, as well as competition or loss experience of the insurance company.

For example, if the insurance company actuaries review a certain area one year and determine that it has a low risk factor and only charges very minimal premiums that year, but then by the end of the year they see a rise in crime, a major disaster, high losses, or claims payouts, it will cause them to review their results and change the premium they charge for that area in the new year. That area will then see rate increases as a result. The insurance company has to do this in order to be able to stay in business. People in that area may then shop around and go somewhere else.

By pricing the premiums in that area higher than before, people may change their insurance company. As the insurance company loses the clients in that area who aren’t willing to pay the premium it wants to charge for what it has determined as the risk, the insurance company’s profitability or loss ratios will likely decrease.

Fewer claims and proper premium charges for the risks allow the insurance company to maintain reasonable costs for their target clients.

How To Get the Lowest Insurance Premium

The trick to getting the lowest insurance premium is to find the insurance company that is most interested in insuring you.

When an insurance company’s rates go too high all of a sudden, it is always worth asking the company whether there is anything that can be done to reduce the premium.

If the insurance company is unwilling to change the premium it is charging you, then shopping around may find you a better price. It will also give you a better understanding of the average cost of insurance for your particular risk.

Asking your insurance representative or an insurance professional to explain the reasons why your premium increases or whether there are any opportunities to get discounts or reduce insurance premium costs will also help you understand whether you are in a position to get a better price and how to do so.

Frequently Asked Questions (FAQs)

How can you lower your car insurance premium?

You can lower your car insurance premium by increasing your deductible.4 Call your auto insurance company and discuss all the ways you may be able to lower your car insurance premium. It may be wise to shop around and get quotes from other companies, too.

What happens if you don’t pay your insurance premium?

If you do not pay your insurance premium, your insurance company could end your coverage. This could happen if you don’t pay your car insurance, health insurance, life insurance, or other insurance premium. You may have a grace period to catch up on premium payments before your coverage is canceled.